Taxation Assignment: Theory, Practice & Law

Question

You are working as a tax consultant in Mayfield, NSW. Your client is an investor and antique collector. You have ascertained that she is not carrying on a business. Your client provides the following information of sales of various assets during the current tax year:

a) Block of vacant land. On 3 June of the current tax year your client signed a contract to sell a block of vacant land for $320,000. She acquired this land in January 2001 for $100,000 and incurred $20,000 in local council, water and sewerage rates and land taxes during her period of ownership of the land. The contract of sale stipulates that a deposit of $20,000 is payable to her when the contract of sale is signed and the balance is payable on 3 January of the next tax year, when the change of ownership will be registered.

(b) Antique bed. On 12 November of the current tax year your client had an antique four-poster Louis XIV bed stolen from her house. She recently had the bed valued for insurance purposes and the market value at 31 October of the current tax year was $25,000. She purchased the bed for $3,500 on 21 July 1986. Although the furniture was in very good condition, the bed needed alterations to allow for the installation of an innerspring mattress. These alterations significantly increased the value of the bed, and cost $1,500. She paid for the alterations on 29 October 1986. On 13 November of the current tax year she lodged a claim with her insurance company seeking to recover her loss. On 16 January of the current tax year her insurance company advised her that the antique bed had not been a specified item on her insurance policy. Therefore, the maximum amount she would be paid under her household contents policy was $11,000. This amount was paid to her on 21 January of the current tax year.

(c) Painting. Your client acquired a painting by a well-known Australian artist on 2 May 1985 for $2,000. The painting had significantly risen in value due to the death of the artist. She sold the painting for $125,000 at an art auction on 3 April of the current tax year.

(d) Shares. Your client has a substantial share portfolio which she has acquired over many years. She sold the following shares in the relevant year of income:

- 1,000 Common Bank Ltd shares acquired in 2001 for $15 per share and sold on 4 July of the current tax year for $47 per share. She incurred $550 in brokerage fees on the sale and $750 in stamp duty costs on purchase.

- 2,500 shares in PHB Iron Ore Ltd. These shares were also acquired in 2001 for $12 per share and sold on 14 February of the current tax year for $25 per share. She incurred $1,000 in brokerage fees on the sale and $1,500 in stamp duty costs on purchase

- 1,200 shares in Young Kids Learning Ltd. These shares were acquired in 2005 for $5 per share and sold on 14 February of the current tax year for $0.50 per share. She incurred $100 in brokerage fees on the sale and $500 in stamp duty costs on purchase.

- 10,000 shares in Share Build Ltd. These shares were acquired on 5 July of the current tax year for $1 per share and sold on 22 January of the current tax year for $2.50 per share. She incurred $900 in brokerage fees on the sale and $1,100 in stamp duty costs on purchase.

(e) Violin. Your client also has an interest in collecting musical instruments. She plays the violin very well and has several violins in her collection, all of which she plays on a regular basis. On 1 May of the current tax year she sold one of these violins for $12,000 to neighbor who is in the Queensland Symphony Orchestra. The violin cost her $5,500 when she acquired it on 1 June 1999.

Your client also has a total of $8,500 in capital losses carried forward from the previous tax year, $1,500 of which are attributable to a loss on the sale of a piece of sculpture which she sold in April of the previous year.

Required: Based on this information, determine your client’s net capital gain or net capital loss for the year ended 30 June of the current tax year.

Question 2 : Rapid-Heat Pty Ltd (Rapid-Heat) is an Electric Heaters manufacturer which sells Electric Heaters directly to the public. On 1 May 2017, Rapid-Heat provided one of its employees; Jasmine, with a car as Jasmine does a lot of travelling for work purposes. However, Jasmine’s usage of the car is not restricted to work only. Rapid-Heat purchased the car on that date for $33,000 (including GST).

For the period 1 May 2017 to 31 March 2018, Jasmine travelled 10,000 km in the car and incurred expenses of $550 (including GST) on minor repairs that have been reimbursed by Rapid-Heat. The car was not used for 10 days when Jasmine was interstate and the car was parked at the airport and for another five days when the car was scheduled for annual repairs.

On 1 September 2017, Rapid-Heat provided Jasmine with a loan of $500,000 at an interest rate of 4.25%. Jasmine used $450,000 of the loan to purchase a holiday home and lent the remaining $50,000 to her husband (interest free) to purchase shares in Telstra. Interest on a loan to purchase private assets is not deductible while interest on a loan to purchase income-producing assets is deductible.

During the year, Jasmine purchased an Electric Heaters manufactured by Rapid-Heat for $1,300. The Electric Heaters only cost Rapid-Heat $700 to manufacture and is sold to the general public for $2,600.

Required:

- Advise Rapid-Heat of its FBT consequences arising out of the above information, including calculation of any FBT liability, for the year ending 31 March 2018. You may assume that Rapid-Heat would be entitled to input tax credits in relation to any GSTinclusive acquisitions.

- How would your answer to (a) differ if Jasmine used the $50,000 to purchase the shares herself, instead of lending it to her husband?

Answer

Using the format given below will help you in drafting the taxation assignment in a descent way. The student consigned us with this task because it was a Taxation Assignment holding very demanding deliverables. In Australia, as per ITAA97 part 3-1 and 3-3, the capital gain tax (CGT) is levied on the disposed of capital assets that attract a CGT event. The net estimated net capital gain for the year is added in the ordinary income as the capital gain is not taxed separately. As per the concept of capital gain and loss recognizing the CGT asset is difficult (Mendoza et al., 2017). According to section 108-5, any property will be determined as a CGT asset, and the equitable and the legal rights are not considered as a property. The assets that are involved in CGT are the property of any type like building and land, units or shares in rights and unit trust, goodwill, interests in partnership assets and partnership assets interest and so on.

a) Block of vacant land

According to section 108-5, the building and land will be regarded as a CGT asset if not utilized for business. CGT asset will be evaluated if the taxpayer disposes of an asset that is determined to be capital assets. The disposed of assets were not purchased before 20th September 1985 (Burkhauser et al., 2015). Therefore, as per section 108-5, the vacant piece of land is a capital asset as the land is not obtained before 20th September thus it is not a pre-CGT asset and not an exempted class of asset.

In the present case, the disposed of vacant land amounting $320,000 as per the current tax year. As per section 110.25 of the Act, the 1st element states that to find the cost of purchase it is essential to consider the cost base of the asset. The land is obtained on January 2001 amounting $100,000 and the under 3rd element the amount of the incurred incidental cost on the land because of the taxes and rates is $20,000 is involved in the cost base. The cost of gain is estimated as follows:

Net capital gain = Cost for the disposal of the asset – the land cost base

= $320,000- (acquisition cost + rates of the council, water bills, and sewerage charges)

= $320,000 – (100,000 + 20,000)

= $200,000

Hence, the net capital gain from the disposal of the vacant block of land is $200,000, as the asset is held for more than 12 months thus, the discount rule that is 50% discount is applicable.

b) Antique bed: According to section 108-5, the collectibles are also regarded as a CGT asset. Collectibles comprise of paintings, antique pieces, collected stamps, jewelry, and manuscripts, hence, in this case, an antique bed is considered as a CGT asset (Jacob, 2018). In the given case the antique bed is stolen on 12th November which is regarded as the disposal date. As per the definition of 108-5, the Louis XIV bed is collectible, and it is not a pre-CGT asset and hence not exempted as it is bought after the cut-off date. As the acquisition cost is more than $500, hence under section 104-20 not exempted from CGT asset.

The taxpayer along with the insurance company complained to claim the total amount, but it was rejected. As per the insurance scheme, the taxpayer was paid a net amount of $11,000. Therefore, from the insurance firm the amount received would be considered as the value of capital disposals and proceeds of the asset. For the incidental and acquiring cost indexation will be done in the following manner:

Index Number of the quarter for sold asset

_____________________________________________ * Base or incidental cost

Index Number of the quarter for purchased asset

- Index number while acquiring the bed that is on 21st July 1986 = 43.2

- Index number while incurred incidental cost that is on 21st October 1986 = 44.4

- Index number while the loss of the antique bed that is on 12th November 2017 = 112.1

Indexation of cost base = 112.1/43.2

= 2.595

Indexation of Incidental cost = 112.1/ 44.4

= 2.525

Net Capital gain and net capital loss from the antique bed

Cost of purchase after indexation = 2.595*3500

= $ 9.082.5

Cost of incidental after indexation = 2.525 *1500

= $ 3,787.5

Total base cost = $ 12,870

Deduction of Capital proceeds from insurance firm = $ 11,000

Net Capital loss = $1,870

Thus, the net capital loss from the antique bed amounts $1,870

c) Painting :Painting is also considered as a collectible item which is bought on 2nd May 1985 which is the base cost for the painting. On 3rd April of the current tax year due to the disposal of the painting the CGT event A1 is attracted. To determine the capital gain and loss, the cut-off date is 20th September 1985, from this it is clear that the asset bought before this dater is exempted from the CGT asset. Therefore, as the painting made a capital gain and attracted the CGT event as it is acquired on 2nd May 1985, it is exempted.

d) Shares : Shares are also determined to be a part of CGT asset, as it is the part of such property that is tangible and intangible. Meanwhile, if the shares are used for business, then they would be involved in the ordinary income as per the provisions of section 6 and are not held part 3-a and 3-b of ITAA 97 (Richardson et al., 2015).

i)Estimation of gain from the sale of shares in Common Bank Ltd share Net capital gain = disposal cost – (amount for purchase + stamp duty)

= (47000-550) – (15,000+750)

= $30,700

ii) Estimation of gain from the sale of Shares in PHB Iron Ore Ltd

Net capital gain = disposal cost – (amount for purchase + stamp duty)

= (62,500-1,000) – (30,000+1,500)

= $30,000

iii) Estimation of gain from sale of shares in Young Kids Learning Ltd

Net capital gain = disposal cost – (amount for purchase + stamp duty)

= (600-100) – (6,000+500)

= ($6,000)

iv)Estimation of gain from sale of shares in Share Build Ltd

Net capital gain = disposal cost – (amount for purchase + stamp duty)

= (25,000-900) – (10,000+1,100)

= $ 13,000

Total net capital gain from the sale of shares = 30,700 + 30,000 + (6,000) + 13,000

= $67,700

e) Violin : As per section 108-5 violin is determined to be an asset for personal use. The asset that is utilized primarily for private use is regarded as a personal asset (Blunden, 2016). In the given case the violin is acquired on 1st June 1999 at the cost of $5,500. Thus, the capital gain made from this asset is disregarded. From the disposal of the violin the estimation of gain is given below:

Net capital gain = amount for the disposal of the asset – the base cost of the asset

= $12,000 – (amount of acquisition + Value of alteration charges)

= $12,000 –$ 5,500

= $6,500

Therefore, on the disposed of antique bed the taxable net capital gain is $6,500.

Estimation of the Net capital gain to be involved in the Ordinary income

The full taxable value of the net capital gain is evaluated in the table given below:

| $ | |

| Net capital gain on the disposal of the vacant plot of land | 200,000 |

| Net capital gain on the disposal of the antique bed | 6,000 |

| Net capital gain on the disposal of shares | 67,700 |

| Net capital gain on the disposal of paintings | 0 |

| Net capital gain on the disposal of the violin | 6,500 |

| Total capital gain | 280,200 |

| Capital loss and set off | 8,500 |

| 271,700 | |

| Discount (50%) | 135,850 |

| The cost to be added in the ordinary income | 135,850 |

Answer 2

In this Taxation assignment we have strictly followed the format given in marking rubrics to cover in helping the student to cover all the deliverables in the assignment Fringe benefits tax of FBT can be termed as the tax that is paid by the employer on the value of benefits that is given to the employees. It can even be described as the non-wage payment or advantage that the employer bestows on the employees. Rapid Heat Pty Ltd is a manufacturer of bathtub who provides some fringe benefits to one of the employees. During the year 2017-18, Jasmine was given a car, loan along with other good that is being manufactured by the company. Hence, in this scenario, Rapid-Heat will be required to pay the FBT. The computation of FBT is shown below:

FBT on the usage of Car:The employer will be subjected to FBT when the car is provided to the employee for usage. In this scenario, the employer needs to pay the FBT. However, if the car does not meet the definition of the car then residual fringe benefits will come into action. Further, there are many other instances when the utilization of car is exempted from fringe benefit. The computation of the FBT on tax can be done in either of the two ways that are the statutory method or the operating cost method. The statutory method of computation of the FBT is utilized because the operating cost method needs the presence of log books with the complete details of the travelling done in terms of kilometres and personal purpose.

In the present scenario, Rapid-Heat Pty Ltd has provided Jasmine with a car on 1st May 2017 that was purchased on the same date for an amount of $33,000. The expenses that are incurred by Jasmine constitutes to $550 on the car that was reimbursed by the company and the car travelled for around 10,000 km. Further, it needs to be noted that Rapid Heat Pty Ltd was unable to utilize the car for a period of 15 days during the year. Hence, in the absence of information, the computation of the FBT will be done as per the statutory method.

As per statutory method

Value of benefit = A*B*C/D-E

Where,

A = Car cost

B = Statutory Percentage

C = vehicle was used for private purpose

D =Days in the Year

E = Contribution of the Employee

The following data were gathered from the case

A = 33000, B = 0.20, C = 320, D = 335 and E = 0

Hence, the computation can be done in the following manner

Value of Benefits = 33000*0.20*320/335-0 = 6,304

Value grossed up = 6304 * 2.1463 = 13,531

Fringe benefit tax on loan:A fringe benefits tax on the loan is chargeable when the employer does not charge the interest or a very low level of interest in charged on loan. When the interest rate is lower as compared to the benchmark rate then the interest rate is considered as a low-interest rate. If the employee owes a debt to the employer and the employee fails to make the payment on time and furthermore, the employer does not ask for the same then it will be treated as a fringe benefit and will be exempt from the ambit of FBT. In the provided case, it is noted that Rapid Heat Pty Ltd has provided jasmine with a loan amounting to $,500,000 at the rate of interest at 4.45%. Out of that, a sum of $450,000 was utilized to purchase a holiday home and the remaining amount was provided to the husband to purchase a share in Telstra without any part of interest. As per the current standard, the threshold rate is 5.95%

Hence, fringe Benefit value on loan = (Bench mark rate – rate charged by employer) * Loan Amount

From the case study we have

Fringe Benefit value on loan = (5.95% – 4.45%)* 500000 * 7/12 = 4,375

Grossed up Value = 4,375 * 1.9608 = 8,579

When the loan is given by the employer to the employee and if the amount is used for the purchase of assets that generates income, such amount is deductible for the FBT computation. However, in the current scenario, the shares are purchased by the husband of Jasmine and hence deduction cannot be claimed by the employer

(a) Fringe benefits tax on goods: An FBT on the goods of the company is chargeable when the company sells the goods to the employee at a price that is lower than the current market price. In such a scenario, the employer will be subjected to pay FBT on the difference that exists in the price at which the goods are sold to the employee

In the present scenario, Rapid-Heat Pty Ltd has sold the goods to the employee (Jasmine) ar an amount of $1300 while the same goods are sold in the market at a price of $2600. Hence, the company will be required to pay FBT on the difference that exists between $1300 and $2600. Hence,

Value of fringe benefit tax on goods = 2600 – 1300 = 1300

Grossed up Value = 1300 * 2.1463 = 4,078

The overall value of fringe benefit tax that i chargeable is as follows:

Grossed up value of Car = 13,531

Grossed up value of Loan = 8,579

Grossed up value of Goods = 4,078

TOTAL = 26,188

FBT charged at the rate of 49% will amount to $ 12,832

(b) Further if Jasmine used the amount of $50,000, the loan that was received by the employer to purchase the share of Telstra then the employer will be entitle for a deduction of interest on the amount $50,000. The new amount of FBT would be as follows:

Value of fringe benefit on loan = (5.95% – 4.45%) * 450000 * 7/12 = 3,938

Grossed up value = 3938 * 1.9608 = 7,721

Now, the total fringe benefit tax that would have been chargeable would be,

Grossed up value of Car = 13,531

Grossed up value of Loan = 7,721

Grossed up value of Goods = 4,078

TOTAL = 25,330

FBT charged at the rate of 49.25% will amount to $ 12,475.

Taxation assignments are being prepared by our accounting assignment help experts from top universities which let us to provide you a reliable assignment help online service.

References

Blunden, H., 2016. Discourses around negative gearing of investment properties in Australia. Housing Studies, 31(3), pp.340-357.

Burkhauser, R.V., Hahn, M.H., and Wilkins, R., 2015. Measuring top incomes using tax record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Burkhauser, R.V., Hahn, M.H., and Wilkins, R., 2015. Measuring top incomes using tax record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Kobestky, M. (2005) Income Tax: Text, Materials and Essential Cases. Sydney: The Federation Press

Mendoza, J.P., Wielhouwer, J.L. and Kirchler, E., 2017. The backfiring effect of auditing on tax compliance. Journal of Economic Psychology, 62, pp.284-294.

Nethercott, L., Richardson, G.,& Devos,K.. (2013) Australian Taxation Study Manual. Oxford university Press

Pratt, J. W. and Kulsrud, W. N. (2013) Federal Taxation. Penguin Publishers

Raymond H. P. (2002) Accounting for Fixed Assets. John Wiley and Sons, Inc

Renton N.E. (2005) Income Tax and Investment, 2nd Ed. Oxford University press

Richardson, G., Taylor, G., and Lanis, R., 2015. The impact of financial distress on corporate tax avoidance spanning the global financial crisis: Evidence from Australia. Economic Modelling, 44, pp.44-53.

Sadiq,K., Coleman, C., Hanegbi, R., Jogarajan,S., Krever, R.,Obst, W., & Ting, A. (2014) Principles of Taxation Law. Sydney.

Corporate integrated reporting

Question

Task:

Description / Requirements: Over the past two decades, corporate social and environmental disclosures have increasingly been made in separate stand-alone reports in addition to a variety of other media such as web sites. These standalone social and environmental reports have become more complex (and long) as a greater range of issues has been disclosed to meet the supposed information needs of a range of stakeholders. More recently, possibly in response to the increased complexity and length of stand-alone reports, there have been moves to recombine some social and environmental disclosures with financial disclosures in single reports. In contrast to earlier social and environmental disclosures made within annual reports, where the social and environmental information was not integrated with the financial information, these recent moves have sought to integrate social, environmental, financial and governance information ( De Villiers et al. 2014*). This new reporting system is referred to as Integrated Reporting . * De Villiers, C., Rinaldi, L., and Unerman, J. (2014), “Integrated Reporting: Insights, gaps and an agenda for future research”, Accounting, Auditing & Accountability Journal, Vol. 27 Iss 7 pp. 1042 – 1067.

Required: You are required to research information on the below issues, and then document the results of your research in an essay format with the following suggested sections: Introduction (suggesting 150-200 words); Body (suggesting 800-900 words); Conclusion (suggesting 150-200 words). 1. In line with the view of the above statement, critically analysis the purpose and necessity of corporate integrated reporting and the theory/ies supporting this type of report. 2. Write a conclusion for your research finding along your opinion on benefits (costs) of for society. Additional information: • You are expected to undertake research in order to complete this task. Review of the above-referred journal article can be a good point to start with. Your research should also include further primary source references i.e. peer-reviewed journal articles, professional publications and scholarly books (avoid Wikipedia type material). • You are required to use a minimum of 6 references (minimum 4 academic journal articles and the other 2 can be from other types of resources e.g. professional publications) to support your discussion. Your references can be included the given article. • Word Limit: 1200 words (excluding references), double-spaced, 12-point Ariel or Times New Roman font. A word count must be included. Students exceeding the word limit by more than 10% will incur a mark penalty. Students must submit a properly referenced assignment that complies with the Harvard referencing style. This includes in-text citations and a reference list.

Answer

Introduction

Corporate Integrated Reporting is a step to make the reporting formats of the companies concise, clear, and more useful. Along with the disclosures in the Financial Statements, there are many other disclosures have been made mandatory for the companies such as social and environmental disclosures. These reports have been made until now in the form of standalone reports that in itself is a very tedious and time taking process. Hence, in order to simplify the reporting pattern of the companies, Corporate Integrated Reporting is being taken into consideration for its implementation (Druckman, 2013). Further, the main benefit that this kind of reporting seeks is that the users of financial statements and reports will understand and anathe lyze the position of the company more quickly and effectively. Corporate Integrated Reporting also was known, as CIR will be a very beneficial tool for every company in saving lots of time and efforts (Slaper & Hall, 2011).

Purpose and Necessity of Corporate Integrated Reporting

The main purposes and aims of Corporate Integrated Reporting are:

1. Providing quality information to the users of financial statements.

The main purpose of switching to Corporate Integrated Reporting is an effort to provide quality information to the users of financial statements. The users include providers of finance/ capital, government, shareholders, banks, creditors, investors, etc. These all are the stakeholders of the company and they have full right to verify the financial position of the company as they have their capital/ funds and reputation attached to the respective company. In addition, clearer the financial reports of the company will be, more will be the capital investment and allocation of capital in the most productive manner (Jorgensen & Soderstrom, 2012). The main purpose of Integrated Reporting included compiling the total information about the company in most useful manner.

2. Enhancement of accountability and answerability.

The integrated corporate reporting aims at enlarging the accountability and answerability through the reports presented by the companies to its users. It is not possible for each user and reader of the financial statement to ask questions from the company regarding the content in financial statements. Hence, the reporting format should be such that it is self-explanatory and clarifies the doubts of the users of financial statements (Eccles & Krzus, 2010). This purpose shall be met out through such integrated reports. For example- when a company seeks financial assistance from the financial institutions and banks, it presents all its reports to the banks. The financial analysts go through all the reports but it might be possible that the finance analyst may not be able to directly understand the financial position of the company and gets confused to the wide range of reports available. Hence, the company may not be able to present its actual financial and nonfinancial position (Pyo & Lee, 2013). Hence, the need of CIR emerges here through which the company can present the material data to the financial institutions and other users through CIR, which would be self-explanatory.

3. Uniformity in viewing and comparing the financial statement.The Integrated Reporting will help the users in comparing and bringing out comparative data that will help them in informed decision-making. The comparison might be of the same company from its preceding years or this might be a comparison with data of other companies in the industry. In case any company which does not use the CIR format will not be a good option when the financial statements of its competitors will be made available for analyzing.

4. Helpful in decision-making.

In case of acquisition or mergers and where CIR reporting is available, the investors and the stakeholders will be largely benefited by having all the financial data at one place and comparison and analysis will be easier because the investors need not consider more database, for example- Annual Reports, Social & Environmental, etc.

5. Non-Financial Data reporting.

Apart from the financial data, CIR will also help in analyzing the nonfinancial data as well as the Human Index and the corporate social rankings which otherwise is not available in the standalone financial statements (Hegarty et. al, 2014).

6. Detection of Key Risks and Key Performance Indicators.

The CIR will also help in finding out the key risks and key performance indicators in the company’s failures and achievements. Key risks may involve the high use of technology, high labor turnover, etc which have to be timely detected and rectified. This will only be possible when such material disclosures are made in the annual presentable reports. Moreover, where the company is aware of key performance indicators which are responsible for the company’s growth and development, the company shall be able to focus largely on those KPIs and invest their time, efforts and money on mainly those KPIs & divert their maximum resources from less productive areas to more productive and profitable avenues (IR, 2016). For example- if a company had 10 kinds of activity/ products out of which four products account for more than 70% of revenue or sales, the company may divert their resources from the remaining 6 products to those profitable products of the company which will help them in earning higher profits (Villiers & Rinaldi, 2014). This kind of material disclosures is expected through CIRs.

7. Display of Inter-Relationship between different reports.

The current corporate reporting formats that include Annual Reports, Financial reports, social and environmental reports, report to shareholders etc are prepared separately and do not show any inter-relationship between each other. The CIR aims to bring entire reporting formats under one roof so that the information that the company seeks to provide to the users may help in the easy understanding of the company operations. In addition, the investors are greatly benefitted because the company CIR format shall provide easy and informed presentable financial and nonfinancial data (Villiers & Rinaldi, 2014). This will allow them to understand the operations of the company easily and restore the faith in the company’s workings.

8. Capital Formation of the companies.

The stability of the stakeholders helps the company to enter into new businesses and it is easy for them to procure funds from the market in the form of bank finance, public offer, debentures, or short-term borrowings (Samaha & Dahaway, 2010). This all leads to steady share prices also.

Conclusion

Before implementing CIR framework, the companies should higher some experts that shall help them in implementing the CIR framework. The whole purpose of CIR reporting is to report and present the data at one place which shall help its users in decision making but it should not be done in a haphazard manner because it may lead to a total disaster because there will always be a possibility that entire data might not be captured or improperly captures by the company which may affect the company’s reputation and will also not help the users of financial statements report.

The CIR may be implemented on a parallel basis along with the standalone statements so that the companies can collect reviews about the same and smoothly convert their reporting process without losing any data and stakeholders faith in the company (Carol et. al, 2016). Therefore, to conclude, it may be said that CIR reporting may be the future of the Corporate Reporting framework and should be adopted by every company to reap the above said benefits of the CIR and pass on its benefits to its users of financial data including the society as a whole?

Reflective Learning Journal Assignment For Conceptual Framework Application In Accounting

Question

Reflective Learning Journal

The purpose of this reflective learning journal is to record and analyse your experiences of learning business accounting as both a process and a product. In your journal you will need to document your thoughts and provide information about what you are learning, how you are learning and your reflections on what you have learned about business accounting concepts and principles. You also need to demonstrate your understanding of the Australian Conceptual Framework for accounting standard setting and the implementation of accounting standard in business practices.

Assessment criteria: The reflective learning journal will be assessed based on the following criteria:

- You need to demonstrate critical engagement with the subject matter including (but not limited to):

- Progressively build up a list of definitions, equations, formulas etc. that need to be memorised and be aware of which will be helpful when recording day-to-day business operations. You can provide explanations of accounting concepts in your own words.

- You can prepare a summary of the knowledge and skills you are developing from topic to topic. Your summary should demonstrate a degree of synthesis and integration rather than being just a list of points.

- You should demonstrate active engagement in learning experiences and activities undertaken, demonstrating the application of accounting principles to practice and/or reinforcement of technical skills.

- Evidence of self-evaluation through progressive assessment tasks (such as practice quiz, weekly exercises or other exercises) completed, how you could have improved your results in quizzes, and in the weekly exercises, and how you plan to make best use of feedback provided for future practices.

- You can make meaningful reflections on the progressive learning experiences, showing how the results of your reflection on learning in earlier topics improved your learning in later topics. Self-evaluations can be a critical part of your learning journey. It is designed to give you the opportunity to reflect and comment on the way you approach assessments, such as quizzes and other tasks.

- You thoughts and comments should be integrated and should be expressed clearly and concisely.

Content: You should focus on one week’s learning materials introduced in weeks 2-6. Please note: don’t try to cover every topic. You can choose to reflect on one particular topic that you are interested, such as cash management.

The topics covering in the reflective learning journal may include, but should not be limited to

double entry accounting, accounting equation, accounting cycle, adjusted trial balance, the use of special journals or subsidiary ledgers, sales and purchases transactions, perpetual and periodic inventory system, inventory costing methods, inventory valuation, internal control, cash management and budgeting, receivables and doubtful debts management.

Answer

Introduction: The character and the functioning of the firm’s function of accounting are defined by the board or the company’s conceptual framework. A conceptual framework is necessary for the ascertainment of the hypothetical and conceptual issues which are adjacent to the firm’s financial reporting system and hence will need a proper and logical foundation which will be helping the firm to strengthen the maturity of the accounting standards.

Conceptual framework prevails in many of the cases but it is specifically designed for financial reporting. It can be called as the statement that is used by the firm to keep data record and assess the philosophy of the firm’s past and maturity of the new ones. Thus the main and foremost function of the accounting is to supply useful information and the basis of the economic decision making.

Conceptual framework’s application

It helps to create benchmarks of concepts and objectives. A firm which is using the conceptual framework should always take into the consideration IASB or FASB standards in order to increase the functionality. The framework should also help to mould the minds of the statement users and make changes in the financial reporting. It should also help the company to compare data from the others. It also helps to solve the problems quickly by the use of the existing basic theories (Singleton-Green, 2016).

It was questioned by the accountants about the mobility of the conceptual framework in the production of financial statements. This was answered by the past history that how the use of conceptual framework has been used by the firm to grow. The accounting standards and the conceptual framework do not work together. They make affects on the income and financial statements of the firm which leads to a contradiction of the transaction details (Baluch et. al, 2011). The standards were made as a reaction to the disgrace or failure or by observing the environment. Their main focus was to improve the approach by introducing new policies.

It could have also been argued that the conceptual framework is having fewer rules and regulations. The management should be led with utmost care and the use of the conceptual framework is thus made necessary. This system will be more rigid and the magnetism of the financial statements will be much more similar compared to the others (IFRS Foundation, 2010).

Objective oriented

The main objective that is needed by the IASB can only be accomplished by the application of the conceptual frameworks thoroughly. These systems have been very useful to the people who are using the financial statements or the new start-ups which are trying to grow in the market. A better and more creative image of the accounting standards has been presented by the use of the conceptual framework. After analyzing the current position of the firm’s financial statements it has been seen that the individual should be provided with the necessary reports that can be utilized by them to ascertain the index of the conceptual framework of the firm (IFRS Foundation, 2013). All the data relating to the liabilities, assets, capital maintenance and expenses should be taken into account while assessing the conceptual framework.

Challenges of the conceptual framework

Conceptual framework proves to be a boon with many advantages but to have a limitation as well. It is well known that the pillars of the conceptual framework are fully based on mind thoughts and this may not seem very practical and successful to other people. For example, the statements of a company can be manipulated in such a way which seems theoretically correct in nature but is practically fraudulent. A conceptual framework has a complicated construction which may appear difficult to many and this can have an impact on the decisions made from person to person while analyzing the reports (Gibson, 2010). The foundations of the conceptual can be seen to depend indirectly on the monetary provisos. Concentration has to be equally divided between both financial and non-financial data by the accounting regulations but it is impossible for the economic apprehensions to impact the decisions of the people while standing alone. As a summary of all the earlier mentioned statements and facts, it is obvious now that one conceptual framework plan is not capable of taking over the market and different people have distinguished thinking and so they require different forms of a conceptual framework to be brought into action. Though Enron, Arthur Andersen were on-time in presenting their company’s financial statements then also they suffered a downfall. By this, it is clear that these companies used their financial statements in a fraudulent way and manipulated them for maintaining the reputation of the company and so it can be concluded from this that conceptual framework has certain limitations (Seilber, 2015). After these incidents, the IASB and FASB have planned to make the conceptual framework and the accounting standards stricter and sent all the rules for change and renovation with the gathered data which includes discrepancies also (Cooper et. al, 2011). These changes have caused the conceptual framework to maintain a higher level which summons the trade-off betwixt reliability, comparability, etc. A perfect sync between the accounting principles will be a boon to the world economy in many ways which are as follows:

- Promoting international transaction and to reduce exchange charges which can be done by delivering honest data.

- To set a level of the data and principles so it can be followed all over the world and is created by multinational policy-makers (Tysiac, 2015).

- By setting an advance system for government accountability.

If the above rules are implemented then it would be seen that international monetary results and money-related management decisions can be made with minimized threats. By setting the above standards it would be seen that the whole world has an equal platform for the accounting policies (Deegan, 2014). All the regulators and auditors will be delivered exactly similar data which would increase their work efficiency.

Conclusion

A conceptual framework has a wide range of advantages and has offered a stiff but precise platform. This platform can be thought of as one to classify and to safeguard social and economic status. Discrepancies which exist in the accounting standards can only be removed by the rules set up by conceptual framework. Easy maintenance of the accounting standard can be done as conceptual framework eliminates the misstatements of accounting standards. It has also been a boon to the preparers, auditors and also to the users of the financial statements.

References

Baluch, C., Cohen, R., Soto, H., Tucker, P., Volkan, A., and Wright, G. (2011) Fair Value Accounting: Current Status And A Proposal For Convergence. The International Business & Economics Research Journal. [onliine]. 10(4), p. 17-29. Available from: https://www.researchgate.net/publication/265411225_Fair_Value_Accounting_Current_Status_And_A_Proposal_For_Convergence [Accessed 27 April 2018]

Cooper, C, Coulson, A and Taylor, P. (2011) Accounting for human rights: Doxic health and safety practices – The accounting lesson from ICL. Critical Perspectives on Accounting. [online]. 22(8), p. 738-758. Available from https://pdfs.semanticscholar.org/29fe/f2147778ed83c4ee682b6e457a70b344a28a.pdf [Accessed 27 April 2018]

Deegan, C. (2014). Financial Accounting Theory (4th ed.). McGraw-Hill: Sydney. Everingham, G.K, Kleynhans, J.E & Posthumus, L.C. (2007) Principles of Generally Accepted Accounting Practice. Juta and Company Ltd.

Gibson, C. (2010) Financial Reporting and Analysis: Using Financial Accounting Information. Cengage Learning.

IFRS Foundation. (2010) Conceptual Framework for Financial Reporting 2010 [online]. Available from http://www.ifrs.org/News/Press-Releases/Documents/ConceptualFW2010vb.pdf [Accessed 27 April 2018]

IFRS Foundation. (2013) A Review of the Conceptual Framework for Financial Reporting: Discussion Paper DP/2013/1. Available from: http://www.ifrs.org/Current-Projects/IASB-Projects/Conceptual-Framework/Discussion-Paper-July-2013/Documents/Discussion-Paper-Conceptual-Framework-July-2013.pdf [Accessed 27 April 2018]

Seilber J. (2015) FASB removes concept of extraordinary, retains guidance on unusual item [online]. Available from: http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-01-fasb-extraordinary-unusual-items.pdf [Accessed 27 April 2018]

Singleton-Green, B. (2016) Discussion of “articulating accounting principles: Classical accounting theory as the pursuit of ‘explanation by embodiment. Journal of Applied Accounting Research. [online]. 17(2), p. 136-138. Available from https://www.emeraldinsight.com/doi/abs/10.1108/JAAR-03-2016-0028 [Accessed 27 April 2018]

Tysiac K. (2015) No more extraordinary items: FASB simplifies GAAP [online]. Available from: http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-201511630.html [Accessed 27 April 2018]

Management Accounting Assignment detailing bookkeeping procedures used by Pacific Telemet Ltd and Go-Go-Grow Ltd

Question

Question 1: Pacific Telemet Ltd. manufactures a high end smart phone with dual sim cards that is popular with business executives who travel overseas frequently. Related financial data for this product for the last year is as follows:

Sales 12,000 units

Selling price $460 per unit

Variable manufacturing cost $184 per unit

Fixed manufacturing costs $360,000

Variable selling and administrative costs $36 per unit

Fixed selling and administrative costs $600,000

The CEO is under pressure from the Board of Directors to increase the profitability of the phones and has asked executives from different departments for suggestions. Three managers have responded with the following ideas:

- The production manager, David Groate, suggests making improvements to the quality of the product. These quality improvements would increase the variable costs by $36 per unit. This would be accompanied by a $60,000 national advertising campaign which he expects would boost sales volume by 30%.

- The sales manager, Kirsten Arnold, believes that the product is unique, but not yet well known enough. Based on her market research, she feels that advertising should be increased by $120,000 and that the product would also be able to bear an increase in price of $60 with sales volume reduced by 12% from the current levels.

- The marketing director, Jess Sutherland, wants to undertake a promotion campaign where a $40 rebate is offered to the first 2,500 phones sold. She expects that the rebate program would boost sales by an additional 2,000 units if spending on advertising was increased by $50,000.

You have been asked by the CEO, Sherri Watkins, to comment on each of these three proposals before she presents them to the Board of Directors. Draft a report in response to this request. You are not asked to make one particular choice or recommendation, but rather to explore the potential strengths and weaknesses that includes discussion on the breakeven, potential profits and, where possible, the margin of safety related to each proposal. Keep in mind that the sales volumes should be treated as estimates only and your report should consider potential variations in actual sales and their effects. Give both qualitative and quantitative support to your comments.

Question 2: You are the accountant for Go-Go-Grow Ltd, a children’s electric toy car manufacturer that is located in Geelong and has customers in Australia and the USA. Their estimated current sales volume is 5,000 units per month and based on this level of production, the company has budgeted the following costs and prices per unit:

Manufacturing Costs per unit (Based on production of 5,000 units per month)

Direct Material Cost $150.00

Direct Labour Cost 75.00

Variable Factory Overhead 35.00

Fixed Factory Overhead 40.00

Total Manufacturing Cost 300.00

Selling & Administrative Costs Variable Selling and Administrative Cost 35.00

Fixed Selling and Administrative Cost 25.00 60.00

Total Cost Per Unit 360.00

Selling Price Per Unit $720.00

Mantel Ltd is an overseas company that sells toy cars all over the world, with the majority of their market to wealthy new parents in China and India. They have approached Go-Go-Grow about obtaining a quote for a special one-off order as they would like to purchase 20,000 toy cars. As this will be a special order sale, there will be no costs incurred for variable selling and administrative costs and no additional fixed costs will be incurred.

This order is because their existing supplier has suffered substantial earthquake damage to their premises, but the CEO of Mantel Ltd also hinted to your CEO that if they are satisfied with the product, this might not be the last deal between the two businesses.

Required:Given this knowledge, what amount should Go-Go-Grow Ltd. bid for this contract in each of the following circumstances:

- The Go-Go-Grow’s annual factory capacity is 90,000 units.

- The Go-Go-Grow’s annual factory capacity is 75,000 units. (To fulfil the order, you may have to pull the product from your regular production)

Assuming that the annual factory capacity is 90,000 units, prepare a report for your CEO explaining your justification for the bid price that you came up with in 1 a). Discuss the possible opportunities and potential disadvantages with accepting this contract with Mantel. Give both quantitative and qualitative support to your discussion.

Question 3 : Describe your own background before you came to do your MBA at Southern Cross University.

How has your earlier educational background influenced your understanding of this subject so far?

When you complete ACC00724, which accounting tools in either Financial or Management accounting do you think will be most useful for your future career? Why?

Answer

Answer 1- Pacific Telemet Ltd.

Specific Telemet Limited is a business organization producing smartphones with dual SIM cards and this product of the company is very popular among the executives that are traveling overseas on a frequent basis. According to the current pricing strategy of the company profits made by the company are as follows-

| Particular | Amount ($) |

| Sales (Units) | 12000 |

| Selling price | 460 |

| Variable cost | 184 |

| Contribution | 276 |

| Contribution (Amount) | 3312000 |

| Variable selling and administrative cost | 432000 |

| Fixed manufacturing cost | 360000 |

| Fixed cost | 600000 |

| Profit | 1920000 |

Board of director has pressurized chief executive officer of the company to increase the sales in an incoming financial year. For this purpose, three managers have proposed two different kinds of strategies. Evaluation of these strategies is as follows-

The strategy of production manager David Groate : Production manager has suggested increasing the overall advertisement expenses by $60,000 along with increasing the quality of products. Increasing the quality of the product will also increase the variable cost by $36 per unit. After this strategy the profitability of the company will increase and revised the statement of profitability is as follows-

| Particular | Amount ($) |

| Sales (Units) | 15600 |

| Selling price | 460 |

| Variable cost | 220 |

| Contribution | 240 |

| Contribution (Amount) | 3744000 |

| Variable selling and administrative cost | 561600 |

| Advertisement cost | 60000 |

| Fixed manufacturing cost | 360000 |

| Fixed cost | 600000 |

| Profit | 2162400 |

On the basis of this profitability statement, it can be said that overall profit generated by the company has increased by 10% as compared to the original profitability of the company. Contribution margin in the given scenario is 52% and total fixed expenses are $1020000, therefore break-even sales would be $1961538. Break-even sales in this given scenario is substantially lower as compared to sales made by the company in the last financial year i.e. $5520000 (Weygandt, Kimmel & Kieso 2015). On the basis of this analysis, it can be said that this proposal is very positive when it is expected to have a positive impact on the overall profitability of the company. There are some weaknesses that should be considered by the chief executive officer before the execution of this strategy. It is important for the company to find an effective method of advertisement so that 30% increase in sales unit can be achieved. It is very difficult for a business organization to increase 30% of its sales within a period of one year only through advertisement expenses (Noreen, Brewer & Garrison 2014).

The strategy of sales manager Kirsten Arnold: The sales manager of the company has read market research and proposed to increase the overall advertisement expense by $120000. This expenses expected to increase the overall price of the mobile phone by $60 but it will also decrease the overall sales unit by 12%. Profitability of the company in this given scenario would be as follows-

| Particular | Amount ($) |

| Sales (Units) | 10560 |

| Selling price | 520 |

| Variable cost | 184 |

| Contribution | 336 |

| Contribution (Amount) | 3548160 |

| Variable selling and administrative cost | 380160 |

| Advertisement cost | 120000 |

| Fixed manufacturing cost | 360000 |

| Fixed cost | 600000 |

| Profit | 2088000 |

It can be seen that the overall profitability of the company has increased by 8.75% if the proposed strategy of the sales manager is implemented. In this case break, even sales would be $2076923 (1080000/52%) which is also substantially lower as compared to current sales of the company. Therefore it can be said that the strategy will also have a positive impact on the profitability of the company. The main problem of the strategies that overall sales unit will decrease substantially i.e. by 12%. This means that the market share of the company will decrease by 12% if this strategy is adopted due to the increase in overall sales price of the mobile phones. Shifting of customers from our business organization to our competitors can have a negative impact on long term existence of the company in the market (Kaplan & Atkinson 2015). It is proposed that this strategy should not be adopted as it would result in a decrease in market share and the increasing profitability is not very substantial as compared to the previous option.

Strategy offered by marketing director Jess Sutherland: According to the marketing director, a new campaign should be started to wear selling price of the product should be lowered by $40 for the first 2500 phones. In addition to that, there will be an advertisement expense of 50,000 towards this campaign and this campaign is expected to increase the overall sales unit by 2000 units. Profitability of the company according to this strategy would be as follows

| Particular | Amount ($) |

| Sales (Units) | 14000 |

| Selling price (on first 2500 units) | 420 |

| Selling price (on remaining 11500 units) | 460 |

| Variable cost | 184 |

| Contribution (on first 2500 units) | 236 |

| Contribution (on remaining 11500 units) | 276 |

| Contribution (Amount) | 3764000 |

| Variable selling and administrative cost | 504000 |

| Fixed manufacturing cost | 360000 |

| Advertisement cost | 50000 |

| Fixed cost | 600000 |

| Profit | 2250000 |

If this is strategy is successful than the overall profitability of the company is expected to increase by 17.18%. The rate of increasing profitability is hired in this strategy if all the three strategies proposed by the different managers is compared. In addition to that additional expenditure on advertisement campaign is also lowest in the case of this strategy. One factor that should be considered by a chief executive officer of the company is the effectiveness of this campaign. Market research can be conducted by the company on whether this strategy expected to have a positive impact on overall sales units of the company or not.

After evaluating all the three strategies it can be said that all of these strategies have a positive impact on the profitability of the company. It is recommended that the management of the company should accept the strategy proposed by the marketing director or production manager (Collier 2015). The strategy proposed by the sales manager should not be accepted by the company as it will result in decreased market share in the industry which will have a negative long term impact on the company. Out of the other two strategies, it is recommended that strategy proposed by marketing director should be accepted because it has increased overall market share of the company by selling 2000 additional mobile units and overall marketing expenditure, in this case, is also comparatively lower.

Answer 2- Go-Go-Grow Ltd

Go-Go-Grow Ltd is in the business of producing children’s electronic toy cars and has customers in Australia and USA. Total demand for these products is around 5000 per month i.e. 60000 units can be easily sold by the company in a particular financial year. Mental Limited is an Overseas company that has a proposed to purchase an order of 20000 toys directly from the company listen to the current demand of products produced by Go-Go-Grow Ltd. this is a special order and there will be no requirement of spending variable selling and administrative cost and the additional fixed cost will also be nil.

(A) When annual factory capacity is 90000 Units

Total demand of the product in the market is 60000 to units and capacity of the company is 90000 units, therefore there is a spare capacity of 30000 unit which can be made by a company without increasing the capacity of the company. Therefore the price charged for every unit of toy car sold to Mantel Limited will be as follows-

| Particular | Amount ($) |

| Direct Material Cost | 150 |

| Direct Labour Cost | 75 |

| Variable Factory Overhead | 35 |

| Total Cost Per Unit | 260 |

Total contract price would be 260*20000= $5200000

Note- there will be no variable selling and distribution cost because this is a direct offer and selling and advertisement is not required (Nagle & Müller 2017).

(B) When annual capacity is 75000 units

Total annual capacity of the company is 75000 unit whereas the total demand in the open market is 60000 units. The remaining capacity of the company is 15000 and company has to fulfill an order of 20000 units to Mantel Limited. For fulfillment of this order, company has to reduce the total number of products sold in open market to 55000 units only and the cost of 5,000 units will be recorded as an opportunity cost in the price charged from Mantel Limited (Langfield-Smith et.al. 2017).

The contract price for 20000 unit will remain the same i.e. $5200000 but the opportunity cost of 5000 units will be added to this contract price. The opportunity cost would be as follows-

| Particular | Amount ($) |

| Selling price | 720 |

| Direct Material Cost | 150 |

| Direct Labour Cost | 75 |

| Variable Factory Overhead | 35 |

| Variable selling and Administrative overheads | 35 |

| Contribution | 425 |

Total contract price= $5200000+ (425*5000) = 7325000

Number of units= 20000

Price per unit= $366.25

Business report

12-01-2019

Chef Executive officer

Go-Go-Grow Ltd

Geelong, Australia

This business report is prepared to explain the price that is determined for the one-off contract offered by Mantel Limited for production of 20000 to units of toy cars in the coming financial year. Currently the annual capacity of the company is around 90000 units and total demand for products in the open market is 60000 units. Therefore there is a spare capacity of 30000 unit which is not currently being used by the company. This is their capacity can be used in order to fulfill the demand of 20000 units by Mantel Limited. Acceptance of this contract will definitely have a positive impact on the profitability of the company and it will also increase possible contracts in the future by this organization.

In the given case, the contract price is established in the same manner as compared to the normal pricing strategy of the company. The only difference, in this case, is that expenses in relation to variable selling and administrative cost are excluded from the product price. This is due to the fact that our business organization is not required to conduct any type of selling and administration cost of these 20,000 units because it will be directly sold to Mantel Limited (Lavia López & Hiebl 2014).

Different business opportunities might arise out of accepting this contract as other business organizations might come with one-off contracts which will be helpful in utilizing the spare capacity of the company. On the other hand the disadvantages of this company is that it might distract out business organization from gaining a substantial amount of market share in the company if these type of contract increases in the future.

Accountant

Go-Go-Grow Ltd

Answer 3- Educational background

My educational background has enables my experience and understanding of the MBA course as Southern Cross University. I have completed the bachelors of commerce degree in the year 2012. This degree of taken from Gujarat University in India and my passing percentage at this course was 64%. In addition to that I have also worked as room attendant in Hotel the Grand Bhagvati and my responsibilities during this job was to assist housekeeping and maintenance department. This experience has provided me knowledge in relation to the manner in which actual business organization operates.

I have studies business administration, accounting and finance during my bachelor of commerce degree. Knowledge acquired from studying these subjects helped me in understanding the MBA course at the university as these subjects are explained in details in MBA course. Combined knowledge of MBA and bachelors of commerce will help me in understanding the financial and management accounting concepts that are being used in actual business organizations. My bachelors of degree will also help in developing an effective and efficient resume after I have completed the MBA. Combination of these degree will help in getting better job opportunities.

Management accounting tool

After completing the assignment ACC00724, it can be said that pricing and costing tools of Management Accounting will be very useful in career development for the future. This is due to the fact that the majority of business organizations struggle to assign proper pricing to the product and services offered by them. By use of these pricing and costing tools, proper direction can be provided to the business organization and it will also very helpful in career development.

Reference

Collier, P.M 2015. Accounting for managers: Interpreting accounting information for decision making. John Wiley & Sons.

Kaplan, R.S. and Atkinson, A.A 2015. Advanced management accounting. PHI Learning.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H 2017. Management accounting: Information for creating and managing value. McGraw-Hill Education Australia.

Lavia López, O. and Hiebl, M.R 2014. Management accounting in small and medium-sized enterprises: current knowledge and avenues for further research. Journal of Management Accounting Research, 27(1), pp.81-119.

Nagle, T.T. and Müller, G 2017. The strategy and tactics of pricing: A guide to growing more profitably. Routledge.

Noreen, E. W., Brewer, P. C., & Garrison, R. H 2014. Managerial accounting for managers. New York: McGraw-Hill/Irwin.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E 2015. Financial & managerial accounting. John Wiley & Sons.

Corporate Accounting Assignment Analysis For Seafarm Group And Woolworths Ltd

Question

Assessment task

Select two public limited companies listed on the Australian Securities Exchange (ASX) that are in the same industry. Go to the website of your selected companies. Then go to the Investor Relations section of the website. This section may be called, “Investors”, “Shareholder Information” or similar name.

In this section, go to your companies’ annual reports and save to your computer your firms’ latest annual reports consecutively for last three years. Do not use your companies’ interim financial statements or their concise financial statements. Please read the financial statements (balance sheet, income statement, statement of changes in owner’s equity, cash flow statement) very carefully. Also please read the relevant footnotes of your companies’ financial statements carefully and include information from these footnotes in your answer.

You need to do the following tasks:

OWNERS EQUITY

- From your companies’ financial statements, list each item of equity and write your understanding of each item. Discuss any changes in each item of equity for your firms over the past year articulating the reasons for the change.

- Provide a comparative analysis of the debt and equity position of the two firms that you have selected.

CASH FLOWS STATEMENT

- From the financial statement of your chosen companies, list each item reported in the cash flows statement and write your understanding of each item. Discuss any changes in each item of cash flows statement for your companies over the past years articulating the reasons for the change.

- Provide a comparative analysis of your companies’ three broad categories of cash flows (operating activities, investing activities, financing activities) and make a comparative evaluation for three years.

- Also provide a comparative analysis of the two companies that you have selected explaining the insights that you can get from the comparative analysis.

OTHER COMPREHENSIVE INCOME STATEMENT

- What items have been reported in the other comprehensive income statement for each company?

- Why have these items not been reported in Income Statement/Profit and Loss Statements?

- Provide a comparative analysis of the items shown in the other comprehensive income statement section for the two companies. If these items were included in the income statement / profit and loss statements of each company, how would the profit attributable to shareholders of the company be affected?

- Should other comprehensive income be included in evaluating the performance of managers of the company?

ACCOUNTING FOR CROPORATE INCOME TAX

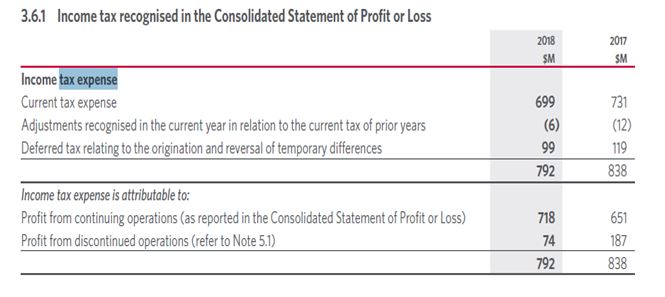

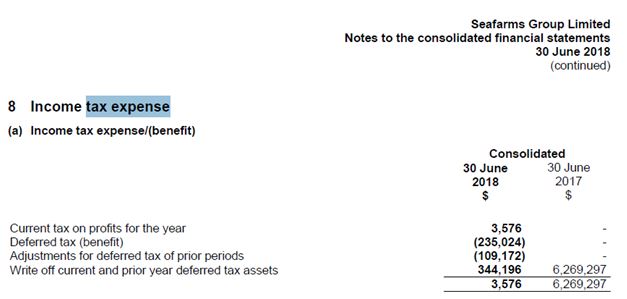

- What are the tax expenses shown in the latest financial statements of the two companies that you have selected?

- Calculate the effective tax rate for both companies that you have selected. Effective tax rate is calculated as (income tax expense / earnings before tax). Which one of the companies has the higher effective tax rate?

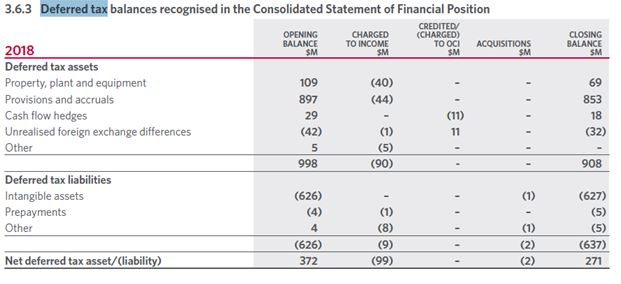

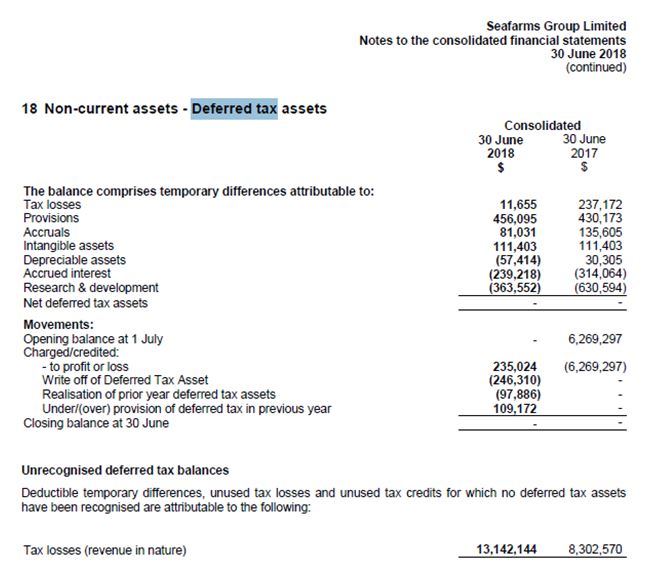

- Comment on deferred tax assets/liabilities that is reported in the balance sheet articulating the possible reasons why they have been recorded.

- Was there any increase or decrease in the deferred tax assets or in the deferred tax liability reported by each of your selected companies?

- Please calculate the cash tax amount for both companies using the book tax amount, changes in the deferred tax assets and deferred tax liability (please do your own research for your better understanding of these concepts and the method of calculating the cash tax amount the book tax amount.)

- Calculate the cash tax rate for both companies. Which company has higher cash tax rate? (Please do your own research to familiarise yourself with how to calculate cash tax rate).

- Why is the cash tax rate different from the book tax rate?

Please remember some aspects of your companies’ treatment of tax can be a very complicated area, particularly for some companies. For a better understanding of the concepts included in the assignment that has not been introduced in the class, please do your own research.

Answer

Executive summary

This report intends to evaluate the financials of two different companies namely Seafarm Group and Woolworths Ltd respectively. The report sheds light on the equity component of the company followed by the income statement, cash flow and other income tax accounting matter. The report further discusses the information about these companies’ equity, comprehensive income statement, statement of cash flow, and corporate income tax accounting tax. To analyse these details thoroughly, the annual report of these companies has been taken into account, and the financials are assessed to observe any variations or alterations in these previously mentioned books of accounts. In addition to these factors, the notes and footnotes to the financial statements of the company have also been taken into due consideration for better understanding. Overall, this report can assist in reflecting enhanced information and comparison betwixt the companies.

Introduction

This report plays a primary role in assessing the details of Seafarm Group and Woolworths Ltd respectively. To Woolworths Ltd, the company has a diversified range of affairs and is also listed on the Australian Stock Exchange. It is a significant player in the Australian retail industry. The reach and availability of the market is high in several segments like gaming pokers, hotel, and liquor.

Nevertheless, the base of customers has been stretched to more than three thousand, and therefore, the company is also regarded as the second largest about revenue. In contrast to this, Seafarm Ltd is primarily an agriculture-based company that is associated with the selling of high-quality seafood and is also registered as a public company of Australia. Furthermore, the company has been involved in several kinds of aquaculture affairs, and it has segregated its issues into three primary segments (Seafarms Group Limited, 2017). Further, last part of the organization is linked to prawn production like black tigers and banana that is sold in the name of Crystal Bay Prawns.?

Owners’ equity

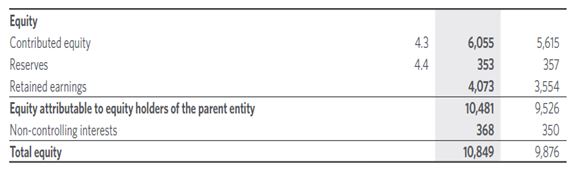

i.) It can be seen from the annual report of Woolworths Ltd that its net equity for 2018 reported at $10849 million when compared to $9876 million in the year 2017. The reason behind this can be attributed to the fact that there are several equity constituents in the company’s financials and the same can be observed from the following table extracted from the annual report. Besides, the company’s contributed equity has also witnessed an increment owing to the issue of fresh shares by it under the program of long-term employee incentives and reinvestment strategies. Moreover, it can also be seen that the reserves have witnessed a decline because of share-based payment costs. Lastly, the alterations in non-controlling interests and retained earnings can be because of enhancement in the company’s net profits even after the dividend payment that was facilitated or undertaken for the shareholders.

In contrast to this, when it comes to Seafarm Ltd, it can be observed that the company’s net equity has witnessed a decline from $327,186,20 in the year 2017 to $158,428,03 in the year 2018 that is a massive deterioration and a negative indicator as well (Seafarms Group Limited, 2017). The fall is observed owing to the alterations in the segment of equity and is further portrayed in the extract from the annual report. Moreover, it can be observed that there has been an increment in the contributed equity and the reason behind this can be attributed to the fact that there was issue of share capital. Furthermore, the retained earnings have depicted a negative figure because of accumulated losses from the past tenures. Besides, there has been an increment in accrued losses that was $199,472,83 that paved a path for the creation of additional retained losses. Lastly, in relation to reserves, the company has witnessed an increment from the last year owing to performance rights that were issued to the employees. This also included lapsed options, share-based payments, etc in the reserves.

ii.) Based on the above analysis, it can be observed that Woolworths is experiencing a better scenario in comparison to Seafarm ltd when it comes to equity and debt position of the companies. This is because Woolworths has better owned capital resources than the latter and is also additionally funded by more of equity and lesser of debt. In addition to this fact, it can be also observed that the company’s investments have enhanced in comparison to the last year. In contrast to this, even though Seafarm is also financed equivalently by debt and equity, yet its ownership has witnessed a tremendous decline in comparison to the last year (Seafarms Group Limited, 2017). In addition, the company’s debt obligations have also witnessed an increment in comparison to the previous tenure that is a negative indicator. Therefore, the company is not in a better position than Woolworths when it comes to equity and debt position.

Statement of cash flow

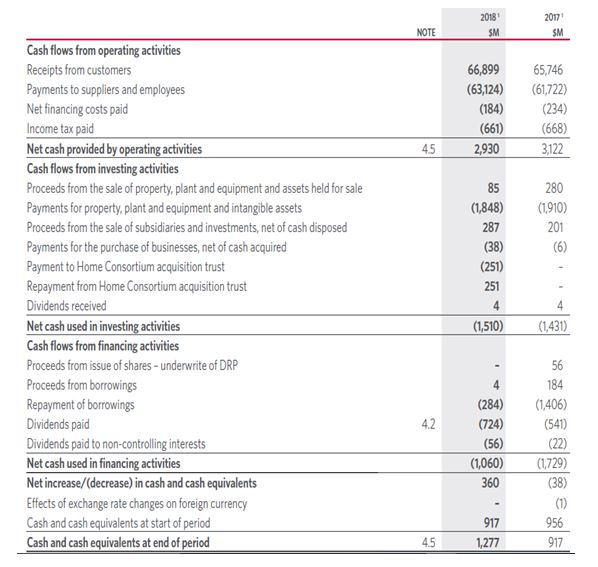

i) It can be seen from the annual report of Woolworths that the company comprises of the following in the cash flow. Firstly, the company’s cash flow from operating affairs comprise of its income and other routine costs that have been incurred during the year. Moreover, this segment has witnessed a decline when compared to the last year and the reason behind this can be attributed to the fact that there have been immense payments to the employees and suppliers in the present year. Secondly, the net cash that have been utilized in the investing activities has witnessed an increment in comparison to the last year. The reason behind this can be attributed to bigger purchases, lesser returns from sale of PPE, etc. Thirdly, the cash utilized in financing activities have been lesser in nature when compared to the last year. Even though there has been dividend increment, yet there has been lesser repayment of obligations in comparison to the last year (Vaitilingam, 2014).

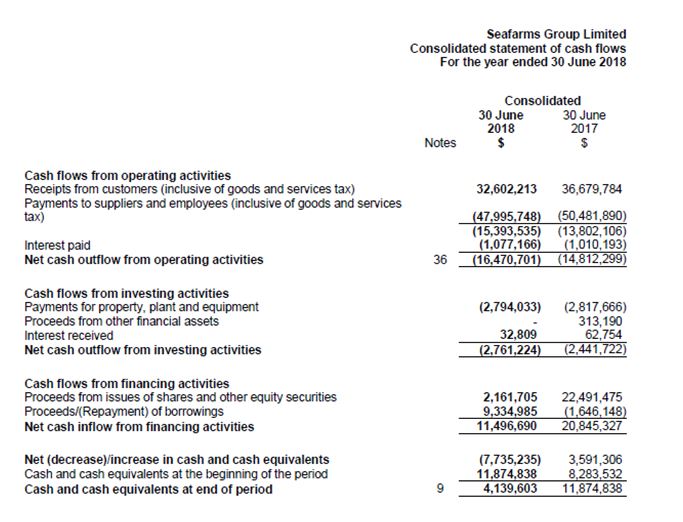

In contrast to the above, when it comes to Seafarm Ltd, it can be seen that there are following segments forming part of its statement of cash flow. Firstly, the company’s cash flow from operating affairs comprise of income and routine expenses that have been incurred during the year (Seafarms Group Limited, 2017). Besides, there has been outflow of net cash and that has enhanced when compared to the last year. Nevertheless, the reason behind this can be attributed to more employee and supplier payments on the company’s part in comparison to customer receipts. Secondly, the company has witnessed an increment in its net cash used in investing activities. The reason behind this is bigger payments for purchase of PPE and nil returns from other financial assets when compared to the last year. Lastly, when it comes to financing activities, the company has witnessed a decline in cash inflow from the same. Even though there has been an immense increase in the liabilities or debts in the present year, yet there has been lesser increase in the returns from the issue of securities and shares. Overall, the net outcome of these activities is that the company has witnessed a decline in its cash and cash equivalent that is a negative indicator.

ii). Comparative analysis

Woolsworth Group Limited: The net cash from operating activities has declined owing to the large payment made to the suppliers and the employees. The reason can be cited owing to huge payment for the business, low proceeds from the PPE in contrast to the last year. When it comes to cash used in financing activities, the cash utilized is low.

Seafarms Group Limited: Cash outflow is observed from the operating activities of the company that enhanced in comparison to the last year due to payments made to supplier and employees. The reasons are due to higher payments for PPE and zero proceeds from other financial assets.

The borrowings has increased to a considerable extent and a small increase in the proceeds from the shares and securities has been noted.

iii). Insight of comparative analysis

Woolworths – Overall, it can be seen that there has been increment in the company’s cash and cash equivalent that indicates better performance and growth in the current year.

Seafarm – Overall, the net outcome of these activities is that the company has witnessed a decline in its cash and cash equivalent that is a negative indicator.

Comprehensive statement of income

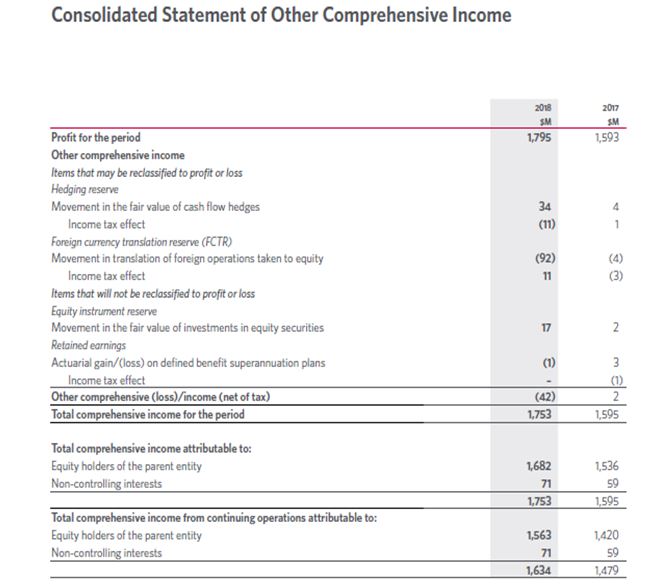

i) vi. There are various items that have been depicted by Woolworths Ltd in its comprehensive statement of income. Firstly, there is movement in equity instrument reserves, secondly there is movement in fair value of income taxes and hedges of cash flows, thirdly there is income tax and translation of foreign currencies thereon, and lastly there is explained superannuation plans losses or gains (Woolworths limited, 2017).

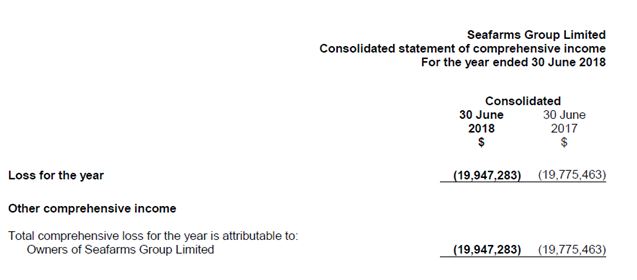

ii) In contrast to the above, Seafarm have not disclosed any details regarding its comprehensive statement of income for the present tenure. This is the reason why nothing is disclosed or reflected in the company’s comprehensive income statement (Seafarms Group Limited, 2017).

iii). The statement of comprehensive income consists of expenses and revenues that have not been realized by the company. Thus, once such transactions are attained, the losses or gains related to the same are identified as realized losses or gains and thereafter, reflected in the income statement. Therefore, the comprehensive statement of income has been alternatively prepared for the sales that have been unrealized in nature (Ross et. al, 2014). Nevertheless, if such income has been reflected in the statement of income, it will reflect that such income which has not been attained has also been depicted in the company’s financials. Moreover, based on the principles of GAAP and IFRS, the total salaries must also be separately disclosed to depict that there are feasibilities of income that can be incurred in the upcoming tenure. However, these must be reflected not inside and instead, outside the statement of income and the reason behind this can be attributed to the fact that such income has not been attained in the present year. In the case of Seafarm Ltd, it can be observed that the company has not prepared or disclosed its comprehensive statement of income during the years. Thus, comparative evaluation betwixt both companies is not feasible in nature.

Moreover, the following items have formed part in the statement of comprehensive income of Woolworths Ltd. Firstly, there is equity instrument reserve that has incurred owing to the revaluation of invested equity securities. In addition, on the disposal of these, the losses or gains attained must be transferred to equity (Power, 2017). Secondly, the company has identified the actuarial losses or gains on the liability of net-defined benefit as and when they occur (Woolworths limited, 2017). Thereafter, these are depicted in the comprehensive statement of income of the company and are not reclassified to such statement of income. Thirdly, the hedge of cash flow is depicted in relation to losses or gains attained based on derivative financial instruments (Porter & Norton, 2014). Lastly, in relation to the variations in foreign currency exchange that has incurred owing to translation of global affairs, planning for the settlement of these transactions have not been made and therefore, have been depicted outside the statement of income.